Markets reacted violently as global economies adopted shelter-in-place policies to combat the spread of Covid-19 earlier this year. Corporate bond credit spreads (or risk premiums), driven by heightened uncertainty and revenue pressure, widened dramatically to reflect the increased risk of downgrade and default. While the magnitude of the sell-off was significant, the direction seemed quite logical given the sudden halt of global commerce.

Since March, financial market performance has been much stronger. Global credit markets have benefitted from significant liquidity support, including low interest rates and direct purchases by central banks of corporate bonds and exchange-traded funds. Sequentially, economic data has also begun to improve. However, many aspects of global economic activity remain far from 2019 levels. At first glance, there appears to be a disconnect between the tighter levels of corporate bond spreads and the weak-but-improving economic picture. With this in mind, we seek to identify what is currently reflected in current corporate bond prices and compare that with our own views.

There are several things a corporate bond spread should compensate for, one of which is the risk of a downgrade. The credit rating from major rating agencies can influence the buying appetite of several market participants, including banks, insurance companies and asset managers. In 2009, rating agencies downgraded $108 billion of debt from investment grade into high yield in the wake of the global financial crisis. Midway through 2020 this previous record of so-called “fallen angels” has been surpassed, with $189 billion of debt downgraded to high yield, including $151 billion in the first quarter alone1

Since the first quarter, the pace of downgrades has slowed meaningfully. We attribute this to the many credit-enhancing decisions management teams have utilised, including dividend and share-buyback cuts, delayed capital expenditures and cost reductions. In addition, the rebound in economic activity and reopening of capital markets have been helpful. While we do not expect a return to the pace of downgrades seen earlier in the year, it is important to note that the risk remains.

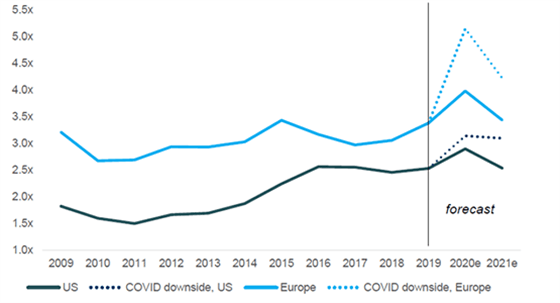

Figure 1 illustrates the gross leverage – debt to earnings before interest, taxes, depreciation and amortisation (EBITDA) – for investment grade companies in the US and Europe that are covered by our internal research team (approximately 80% of the universe of global investment grade corporate bonds). It also includes our forecasts for our base case and “Covid downside” scenarios. The latter includes assumptions on a much slower pace of activity driven by additional waves of infection (a so-called “L- shaped” recovery). It is important to note that in that scenario leverage rises sharply by the end of the year, a development that would likely coincide with another raft of ratings downgrades.

Figure 1: Gross leverage

Source: US Department of Labor/Columbia Threadneedle Investments, 21/3/2020

Defaults

As of 30 June, the trailing 12-month default rate for US high yield bonds stood at 6.19%2, the highest in 10 years. Our internal default forecast for the next 12 months currently stands at 8.5%, indicating a trend of further deterioration from June, as the demand destruction of the pandemic impacts the most highly levered companies.

While our forecast is not perfect, we find it helpful to compare it to what is implied by current market prices. At mid-year, the yield spread on the Merrill Lynch High Yield Index stood at 6.46% above Treasuries. We can divide that spread into two components, a liquidity premium and a default premium. If we assume a long-term average liquidity premium of 3%, this leaves 3.46% to compensate for default risk. With some simple recovery assumptions3, this implies the market is pricing in a default rate of about 5.5%. At first glance, this seems worrying given our much higher default expectations.

However, let’s revisit the liquidity premium. It may not be fair to assume investors should earn an “average” liquidity premium in this market. The sheer quantity of liquidity provided by central banks is enough to challenge this assumption. The US Federal Reserve alone has $485 billion in fresh equity capital from the US Treasury4. It has used a leverage ratio of 10x in measuring its asset purchase ability for credit assets. So, in rough terms the Fed has enough firepower to purchase $4.9 trillion in corporate bonds – roughly half of all US investment grade bonds, high-yield bonds and leveraged loans combined. Given the scale of that liquidity, we can assume the liquidity premium has compressed.

Therefore, if we assume investors are now compensated for a 1% liquidity premium in high yield, this implies the market is actually pricing in an 8.7% default rate for the market, slightly above our forecast. Stirring this together, we think the market is pricing in both an elevated default rate and continued support from the Fed in the year ahead. While we directionally agree with that, it places an increased importance on credit selection to mitigate default risk today, given the skinnier cushion in spreads.

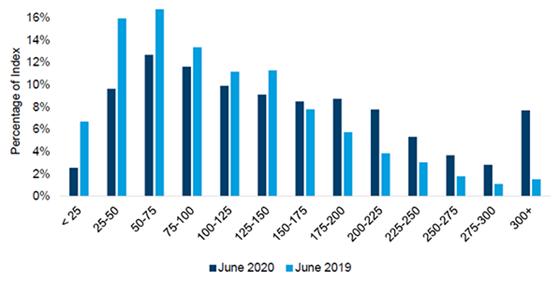

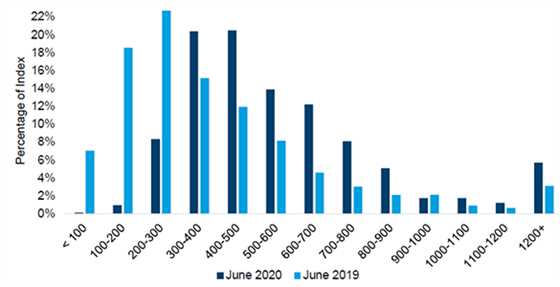

Dispersion

As of 30 June the average credit spread on the Bloomberg Barclays Global Aggregate Corporate Investment Grade and the Bloomberg Barclays Global High Yield indices was 156 bps and 646bps respectively5. However, it is becoming more difficult to find an “average” bond. For example, less than 25% of the high yield index trades within 100bps of the average (560-760 range). Figures 2 and 3 illustrate the dispersion of credit spreads across these two markets. As economic uncertainty has increased, the dispersion has widened noticeably. This distribution illustrates the market’s differentiation of the universe based on potential risks, including the risk of downgrade, default, or anything else.

We believe such a wide distribution of prices also creates opportunity for an active manager. A wider distribution can allow for the construction of a portfolio with very different risk and return characteristics than a broad index.

Figure 2: Yield spread dispersion, Bloomberg Barclays Global Aggregate Corporate Index

Source: Bloomberg Barclays, Columbia Threadneedle Investments, as at 30 June 2020

Figure 3: Yield spread dispersion – Bloomberg Barclays Global High Yield Index

Source: US Department of Labor/Columbia Threadneedle Investments, 21/3/2020

Global central banks have been actively supporting corporate bond markets. In the US, the Fed is even purchasing some high yield bonds. This has helped create strong technical support for the market. While central banks can help to solve the liquidity issues markets were facing earlier in the year, they cannot cure solvency issues. Downgrade and default risk will remain heightened if economic re-openings are slow and uneven.

As a result, the market now reflects a risk premium that is higher and more widely distributed than last year. This creates an opportunity for strong credit research to sift through noisy data and identify companies that can weather the storm. With risk-free rates likely to remain low for the foreseeable future, the opportunity to generate income from a risk-managed credit allocation remains compelling.